Recovery plans in the European Union and the Spanish state and its implications for energy and climate policy

The measures taken to deal with the health emergency and the spread of COVID-19 have brought an unprecedented economic slowdown. As a result, public institutions have activated plans, mechanisms and instruments that are intended to stop the shock, reactivate the economy and return to pre-pandemic normality. In this context, large companies are playing a role similar to that of the banks during the financial crisis of 2008: at a time of high uncertainty they are benefiting from public policy and are being rescued.

At European level, we see that the two financial institutions that have been responsible for carrying out this task have been the European Central Bank (ECB) and the European Investment Bank (EIB). In the case of the ECB, in 2014 it created the Quantitative Easing (QE) program to respond to the financial crisis of 2008. The mechanism used consist in buying assets to purchase debt from the countries of the euro zone and the purchase of corporate bonds, from which more than 300 large companies have benefited, including BMW, E.ON, Enagás, ENEL, ENI, Peugeot, Renault, Ryanair, etc.

On March 24, 2020, as a result of the economic impacts generated by measures implemented to contain COVID-19, such as border closures and lockdowns, the ECB authorized1 an extension of the program with 750 billion euros, called the Pandemic Emergency Purchase Programme (PEPP)2. The process of selecting the beneficiary companies is delegated to the central banks of Germany, France, Spain, Italy and Belgium, and the eligibility criteria they use are the financial stability of the company and the quality of the debt3.

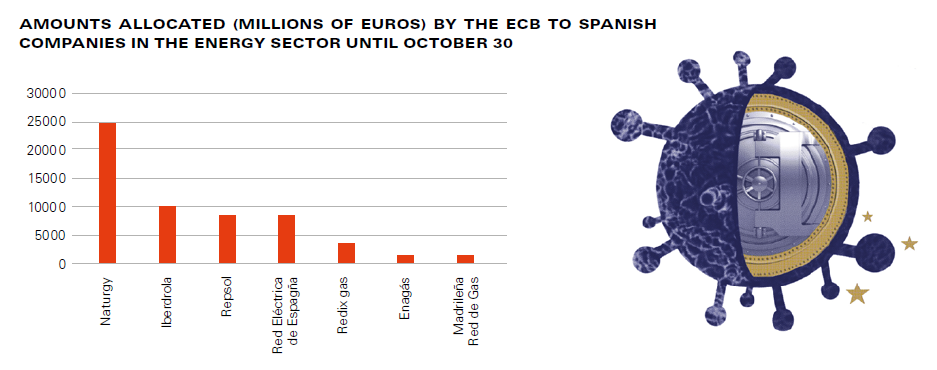

The very concept of the PEPP means that it is only available to large companies. Bond issues have costly procedures and are only made for amounts ranging from hundreds of millions to billions of euros. Furthermore, the eligibility criteria for bank intermediaries do not include any exclusion or conditions on social, environmental or climate aspects and ‘there will be no positive or negative discrimination on the basis of the economic activity of the issuing entities’, which is why large companies like Total, Airbus, Shell, E.ON and more than 50 transnationals are benefiting. In the case of the energy sector, Spanish companies have been granted with 58 billion of euros until October 30th, where Naturgy, Iberdrola, Red Eléctrica de España and Repsol stand out.

The EIB, the public investment bank of the European Union (EU), will also play an important role in the recovery plans for the pandemic. On the one hand it has created an emergency package of 40 billion euros4 and a guarantee fund of 25 billion to mobilize private capital worth 200 billion euros5. These two mechanisms will be used to facilitate loans, by means of guarantees, and by guaranteeing small and medium sized enterprises (SMEs). It should be noted that the processes established are not very democratic and not very transparent, since information from financial entities is only provided if the promoter has not presented legitimate reasons for confidentiality. Furthermore, they do not take into account any environmental and social criteria, which contradicts the energy policy approved for the coming years6 and its self-claim as a climate leader in the public finance sector, through the Climate Bank Roadmap 2021-20257 .

How has it developed in the Spanish state?

Transferring it to the Spanish state, the EIB has approved a loan of 1.5 billion euros8 for the Instituto de Crédito Oficial (ICO), which is the public bank in charge of providing liquidity to private banks so that they can lend money to companies and freelance workers. This body was created in 1971 and is attached to the Ministry of Economic Affairs and Digital Transformation.

The ICO has also been the body in charge of managing the mechanisms and instruments approved by the Spanish government to stimulate economic recovery during the lockdown caused by COVID-19. These mechanisms have been: 1) the guarantee for short-term loans9; 2) the purchase of promissory notes10 from companies; and 3) guarantees for promissory notes11. Other indirect aid to companies has also been created, such as public contracts awarded by emergency means without prior tender, through public-private partnerships (PPPs)12 , as well as aid from city councils and autonomous communities.

A first wave of guarantees and purchase of promissory notes took place between March and June, when the Spanish government assigned them an amount of 100 billion euros. At the beginning of July a new line of investment guarantees for enterprises was announced, amounting to 40 billion euros, and another one of 10 billion euros for a fund aimed at guaranteeing the solvency of strategic enterprises through the purchase of shares13, managed by the state-owned holding company Sociedad Nacional de Participaciones Públicas (SEPI), which is the strategic instrument attached to the Ministry of Finance for guaranteeing that the activities of the enterprises and sectors are in line with the Government’s policies14.

In parallel with the process of the guarantees and the purchase of promissory notes awarding, in the Spanish Congress of Deputies was created the Comisión para la Reconstrucción Social y Económica. Its purpose was debating and determining which measures should be taken in the areas of health, European Union, social and economic issues which would allow a recovery of the multidimensional crisis generated by the COVID-19. The Congress voted the conclusions of each area on July 29, where the conclusions of the social area were not approved, but it was for the areas of health, European Union and economy.

The devil is in the details

The loans and financial support offered by the ICO are usually managed through the large Spanish commercial banks such as Bankia, BBVA, Caixabank, Santander and Banc Sabadell, among others. The role of intermediaries places them as the greatest beneficiaries of the process because it allows them to make a profit through the margin that exists between the interest on the credit they obtain from the ICO and the interest they set on the loans they offer to companies.

With regard to the guarantees and purchase of promissory notes approved by the Spanish government to deal with the impacts generated by COVID-19, three negative elements can be identified: 1) Risk of public debt: the government, through the ICO, assumes the non-repayment of the funds received by the companies through the general budget; 2) Lack of conditionalities: the beneficiary companies are required not to have their headquarters in a tax haven, allowing their subsidiaries to have one15, nor to distribute dividends for an unspecified period of time; and 3) Lack of transparency: the information published on the ICO’s website and official government channels does not state which companies have benefited, the amount granted or by what mechanism. Some of the beneficiated companies have been known by researching their press releases and news, since they are obliged to publish any relevant loan operation.

It should be noted that 30% of the total amount of guarantees and purchase of promissory notes was intended to benefit large companies. The lack of exclusion criteria and social, environmental, climatic and employees rights conditions has allowed companies in the sectors that have contributed most to global warming, that have a history of ecological, climatic, social, gender and/or revolving door impacts, that have subsidiaries in tax havens and/or that have been decapitalized by distributing large dividends to their shareholders in recent years16, to have access to these grants. This has been the case of Iberia, Vueling, OHL and NH Hoteles.

The conclusions of the economic area of the Comisión para la Reconstrucción Social y Económica could have included part of the exclusion criteria and conditionalities to deal with the impacts set out in the previous paragraph, since different parties in the Spanish Congress of Deputies, including those in government, PSOE and Podemos, gave their support to an amendment that included them. Few days later PSOE withdrew its support to the amendment, but the distribution of dividends was the only conditionality not included in the economic area conclusions. Although it would not be possible for these eligibility criteria to be applied in the mechanisms and instruments approved in the first wave of aid, with an amount of 100 billion euros, they can be applied in future enlargements and created later17.

A public consultation process was also carried out so that citizens and interested parties could make their contributions, but none of the proposals have been incorporated.

What should rescues look like to ensure a fair socio-ecological transition?

The amendment presented in the conclusions of the economic area of the Comisión para la Reconstrucción Social y Económica was in part the result of joint research by the Observatori del Deute en la Globalització (ODG), Ecologistas en Acción and the Observatorio de Multinacionales de América Latina (OMAL), which culminated in a communication and advocacy campaign in the weeks before the vote in the Spanish Congress of Deputies18.

The main complaint was that it was considered disproportionate that such an amount of resources be allocated to companies to the detriment of the financing necessary to ensure welfare, social protection and the implementation of socio-ecological transition measures.

In addition, the granting of aid from the ECB and the ICO to polluting companies establishes a link between the two parties. This alliance implies that financial institutions want to guarantee the viability of the fossil fuel sector so that the aid is returned, which puts at risk the achievement of a fair social-ecological transition in the short term.

The lack of exclusion criteria and conditionality in social, environmental, climate and labor aspects in the bailouts to companies in the fossil fuel sector is an obstacle to achieving the objectives of the Paris Agreement. These rescues also clash with the Plan Nacional Integrado de Energía y Clima (PNIEC) 2021-203019 approved by the Sapnish government, which sets the following objectives for the end of this decade: 1) to reduce emissions by 23% with respect to 1990; 2) 42% of energy must come from renewable sources; and 3) to improve energy efficiency by 39.5%.

The demands contained in the campaign called for bailouts to guarantee a just socio-ecological transition and therefore should be: 1) transparent; 2) fair; and 3) effective. It should be noted that these demands have been elaborated taking into account the context of the Spanish state, but they can be extrapolated to the realities of different countries and territories.

In order for the economic bailouts to be transparent there must be public scrutiny. This must be done by publishing the name of the companies that have benefited from public funding, their amount and conditions on the website and in the annual reports of the public body. The number of meetings held between company representatives and administrations should also be published. In addition, it is necessary to create independent bodies for supervising aid and the companies that benefited.

A fair rescue involves prioritizing aid to those companies whose activity contributes to a fair socio-ecological transition and a change in the model of provision and management of services and goods. Therefore, companies that do not meet the following criteria should be excluded from aid:

- Climate: sectors whose activities increase the magnitude of the climate crisis and do not contribute to compliance with the Paris Agreement, such as the fossil fuel, aviation or the automobile sector

- Environmental: companies with a history of reporting impacts on resources, biodiversity and complaints about pollution

- Human rights: companies in breach of human rights legislation and/or with open processes in international human rights courts

- Social and gender: companies in sectors with negative social impacts, such as armaments or offering precarious conditions to workers

- Financial: companies with substantial profits and/or have recently distributed extraordinary dividends, groups involved in or convicted of corruption or serious economic crimes and which have subsidiaries in tax havens.

Companies that are eligible for bailouts must be required to comply with social, gender, environmental, climate and work clauses in order for the bailout to be effective. These conditions are:

- To draw up an emissions reduction plan in line with the Paris Agreement

- To prohibit the distribution of dividends until the aid is fully repaid

- To accept a certain amount of control by the Spanish state and workers including them in the Board of Directors until the aid is repaid

- Prohibit staff restructuring or layoffs for six months after full repayment of the aid

- To limit the maximum remuneration of the company’s executives

- To waive the right to sue the Spanish state

- To pay taxes in the Spanish state.

References:

1. Approval Pandemic Emergy Purchase Program: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32020D0440

2. Pandemic Emergency Purchase Program: https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html

3. Pandemic Emergency Purchase Program elegibility criteria: https://www.ecb.europa.eu/mopo/implement/omt/html/cspp-qa.en.html

4. EIB Emergency package: https://www.eib.org/en/press/all/2020-086-eib-group-will-rapidly-mobilise-eur-40-billion-to-fight-crisis-caused-by-covid-19

5. EIB Pan-European Guarantee Fund: https://www.eib.org/en/press/all/2020-126-eib-board-approves-eur-25-billion-pan-european-guarantee-fund-to-respond-to-covid-19-crisis?utm_source=twitter&utm_medium=Social&utm_campaign=PressRelease&utm_content=na&cid=Social_twitter_PressRelease_2020-05-26-12_en_na_na_na

6. EIB Energy Lending Policy: https://www.eib.org/attachments/strategies/eib_energy_lending_policy_en.pdf

7. EIB Climate Roadmap 2021-2025, position paper: https://www.euractiv.com/wp-content/uploads/sites/2/2020/06/final_eib_group_cbr_position_paper_15_06_2020.pdf

8. EIB loan to ICO: https://www.eib.org/en/projects/pipelines/all/20200190

9. Guarantee for loans of companies and freelance workers, up to 5 years.

10. Debt that a company issues to finance itself and undertakes to repay the amount with the interest stipulated with the issuer. Similar to a bond, but with shorter terms.

11. Investors buy the debt issued by the company and the ICO acts as guarantor.

12. Definición colaboraciones público-privadas: https://odg.cat/es/colaboraciones-concesiones-publico-privadas-cpp/

13. El País: https://elpais.com/economia/2020-07-02/el-gobierno-lanzara-una-nueva-linea-de-avales-de-40000-millones-para-financiar-la-economia-digital-y-la-ecologica.html

14. SEPI: https://www.sepi.es/en/get-know-sepi/who-we-are

15. La Marea – YoIbextigo: https://www.yoibextigo.lamarea.com/informe/noticias/ibex-35/acciona-melia-ferrovial-ertes-y-paraisos-fiscales-en-el-ibex-35/

16. Op-letter sent to Spanish Deputies: https://odg.cat/es/prensa/carta-diputados-rescates/

17. 20 Minutos: https://www.20minutos.es/noticia/4313520/0/el-psoe-suprime-las-condiciones-para-rescatar-empresas-que-habia-apoyado-dos-dias-antes/?autoref=true

18. Communication and advocacy joint campaign ODG, Ecologistas en Acción and OMAL: https://odg.cat/pagines_campanyes/rescates-covid19/

19. Plan Nacional Integrado de Energía y Clima (PNIEC) 2021-2030: https://www.idae.es/informacion-y-publicaciones/plan-nacional-integrado-de-energia-y-clima-pniec-2021-2030

With the support of: